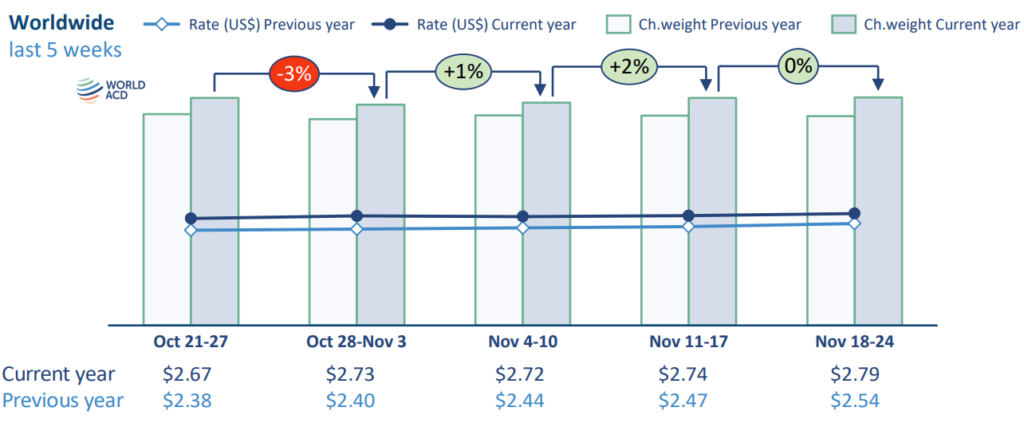

In the final week of November (week 47), global air cargo tonnages remained stable compared to the previous week, while rates continued to rise, reaching the highest levels of 2024. According to WorldACD Market Data, global average rates increased by 2% week-on-week (WoW) to US$2.79, driven by rising spot rates from North America (12%) and Europe (8%). Average global spot rates climbed 4% WoW to US$3.21, while contract rates saw a slight decrease (1%) to US$2.65.

Year-on-year (YoY), global rates were up 10%, with spot rates surging 22% and contract rates rising 8%. Among origin regions, Asia Pacific and the Middle East and South Asia saw stable weekly rates but posted substantial YoY increases of 8% and 46%, respectively. Notably, North America showed strong WoW growth but remains the only region with rates below 2023 levels.

Chargeable weight displayed mixed trends. While tonnages were flat overall, Central and South America recorded a 3% WoW increase, and YoY chargeable weight was positive for all regions except Africa (-3%). North America led YoY growth at 22%, driven by the timing of Thanksgiving, which fell one week later this year compared to 2023.

Capacity adjustments are influencing rate trends.

On Transatlantic routes, capacity fell by 3% YoY, primarily due to a 10% reduction in freighter capacity, while belly capacity held steady. Conversely, capacity on Asia Pacific–North America routes grew 7% YoY, reflecting increased demand for e-commerce shipments.

The shift of freighter capacity from the Transatlantic to Asia Pacific has dampened rate increases in some lanes, particularly from China to the USA, where average rates declined 3% YoY. Additionally, more forwarders secured capacity in advance, muting the typical peak season rate surge seen in prior years.