IBA, the aviation intelligence and advisory company, has warned that the collapse of Spirit Airlines may signal broader stress across the low-cost carrier (LCC) sector, with the airline’s financial position deteriorating sharply in the year leading up to its failure.

Data from IBA’s Insight aviation intelligence platform found that, in 2025, the airline reported a net loss of US$2.8 billion and an EBIT margin of -23.6%. At the same time, it recorded a widening gap between Revenue per Available Seat Kilometre (RASK) and Cost per Available Seat Kilometre (CASK) of -1.4 cents per ASK, underlining structurally negative unit economics prior to its collapse.

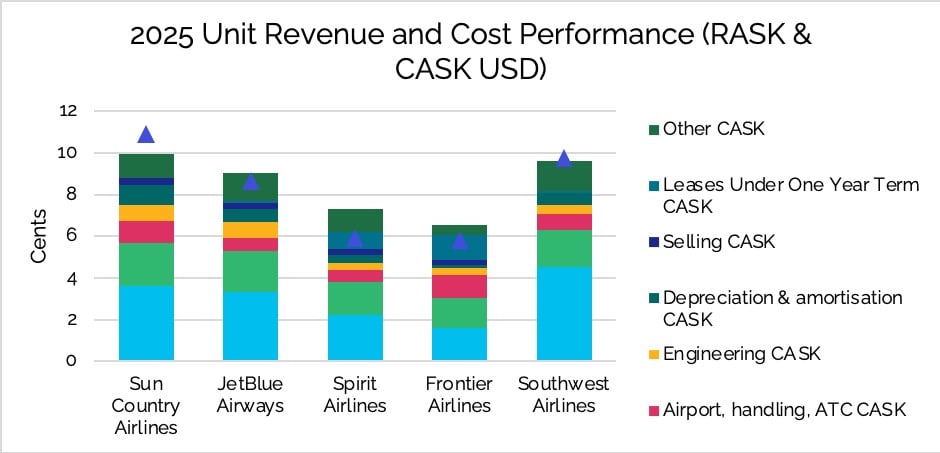

IBA’s analysis of the airline’s unit revenue and cost performance indicates that Spirit lost its cost advantage relative to competitors in 2025, before the recent rise in fuel prices. The chart above shows that, compared with other US low-cost carriers — including Southwest Airlines, JetBlue Airways, Frontier Airlines and Sun Country Airlines — Spirit’s cost base had moved closer to competitors and, in the case of Frontier Airlines, exceeded it, eroding the core ULCC cost differential.

IBA’s assessment shows that, by the time Spirit Airlines ceased operations on May 2, it operated a fleet of 114 Airbus narrow-body aircraft with an average age of 7.0 years. Approximately 83% of the fleet was leased.

IBA highlights that, while fuel acted as the final trigger, it was not the root cause of the airline’s collapse. Spirit’s financial position had already weakened significantly, with negative operating cash flow of US$930 million and a structurally negative unit margin, leaving little capacity to absorb further increases in operating costs.

The strategic challenge for Spirit was that its ULCC model did not operate within a protected niche. The airline competed directly with US legacy carriers across much of its network, with only around 6% of capacity on exclusive routes, exposing it to sustained pricing pressure from airlines with stronger distribution, loyalty programmes and greater schedule depth.

IBA notes that the wider implication is that Spirit may not be an isolated case. Airlines with high lease exposure, limited fuel hedging, weak liquidity and sustained negative unit economics are becoming increasingly vulnerable in the current operating environment, particularly if fuel prices remain elevated or further external shocks emerge.

Dan Taylor, Head of Consulting at IBA, said: “Spirit Airlines’ collapse reflects a structural breakdown in its cost model rather than a single external shock. Airlines with lease-heavy fleets and limited pricing power are particularly exposed when cost pressures rise, especially if the underlying unit economics have already deteriorated. In this environment, the combination of negative margins and limited financial flexibility can quickly become unsustainable.”