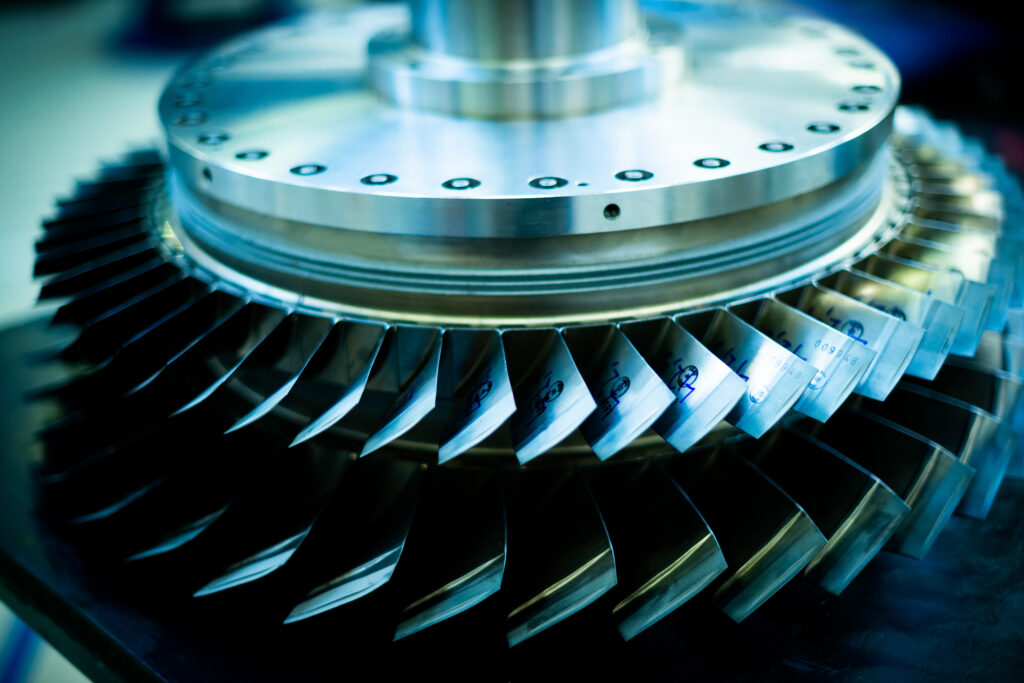

The different challenges faced with life limited parts (LLPs) because unlike other engine parts, LLPs cannot be “repaired,” “refurbished,” or “overhauled” to extend their life once they reach their certified limit.

With the cost of a jet engine for a commercial aircraft like the CFM LEAP or P&W GTF families running well into eight figures, it is hardly a surprise that the cost of engine maintenance is also hugely expensive. Consequently, carriers and MRO operators are both constantly looking for ways to reduce these costs, but the problems faced are exacerbated by the fact that there are generally two types of part for an engine. First, you have parts which are repairable, which can be overhauled, and which can have their lifespan extended through careful maintenance. Then you have your life-limited parts, or LLPs as they are known. These are parts which are manufactured to a specific design, using approved materials, and while requiring maintenance, this cannot extend their lifespan as this is predetermined in terms of cycles or hours used. So, already you can see one of the main challenges, as when do you choose to replace an LLP when shop visits rarely coincide exactly with their expiry. Similarly, when an engine is nearing its lifespan, it makes little sense to use costly brand-new LLPs that will outlast the engine. Fortunately, the market for ‘green time’ LLPs seems to help overcome a number of problems.

To learn more about the effective management of life limited parts we approached several specialists in the field of engine MRO and quizzed them further on the challenges they face.

How does LLP planning influence engine shop visit timing?

We wanted to establish just how important the lifespan of LLPs is to the overall maintenance schedule of aircraft, and the problems created if it is not successfully factored into the equation.

LLP planning shapes shop visit timing because LLPs set the hard cycle limits that ultimately dictate when an engine must come off wing. As the lowest remaining cycle part in the stack approaches expiry, it becomes the primary driver of removal timing—often overriding performance health, EGT margin, or other technical indicators. For smaller and midsize operators and lessors, this creates a fixed window in which a shop visit has to occur, which can compress planning horizons and force earlier than ideal removals. Virgil D Pizer, CEO, Pem-Air Turbine Engine Services goes on to explain further: “LLP status also influences the type of visit that makes sense. When an aircraft has several years of service ahead, operators may justify a full restoration and full or partial LLP stack replacement. When the aircraft is closer to phase out or lease return, a lighter, module-focused visit—or even a green-time engine—can be more economical than investing in high value LLPs. Because LLP exposure affects both cost and remaining life, it becomes a central factor in deciding whether to restore, defer, or pivot to an alternative strategy. Unscheduled removals add another layer of pressure. If an engine with limited LLP life suffers an unexpected event, operators may be forced into an early shop visit that accelerates LLP spend and disrupts fleet availability. With smaller fleets and limited spare coverage, this can have an outsized operational and financial impact. Lessors feel the same timing pressure from the other side: LLP cycles remaining influence mid-life lease pricing, redelivery conditions, and asset value protection. As a result, LLP planning often determines not just when an engine is removed, but how the asset is positioned for the next lease cycle.”

In the opinion of Dave Hobbs, VP Sales, AerFin, “Life Limited Parts (LLPs) sit at the centre of engine maintenance planning. With fixed cycle limits set by the OEM, they create non-negotiable deadlines that operators must work around. In practice, the goal is to align LLP replacement with scheduled shop visits – whether that’s for performance restoration or a full overhaul. Done well, this avoids the need for additional, unplanned maintenance events. If LLPs aren’t aligned properly, the impact is immediate. Engines can be forced off wing earlier than expected, or require incremental shop visits, both of which drive up cost and disruption.” He then concludes that: “Effective LLP planning focuses on balance. By managing the consumption of LLPs across the engine, operators can maximise time on-wing and extract full value before removal.” Dag Johnsen, COO, Aero Norway is of a like mind, highlighting the criticality of optimum engine life and shop visit timing. He tells us that: “LLP management is not just compliance, it controls shop visit cost, engine availability, and asset value. Those operators who manage LLPs proactively spend less and extract maximum life out of every engine. From Aero Norway’s perspective as a CFM56 engine specialist, LLP planning is less theoretical and much more operational, it directly drives induction timing, workscope design, and ultimately shop profitability. For a CFM56 engine (whether -5B/-5C or -7B), LLPs are often the primary drivers of EGT margin strategy in the hardware. The goal is to provide the optimum engine life and shop visit timing, not just performance deterioration. Shop visits are planned around ‘hard LLP limits’ in the HPT/LPT disks and shafts. If LLPs are nearing expiry, we’ll work with our airline customers to find ways to advance a shop visit even if the engine is still performing. Conversely, if LLP life is strong, we can find ways to extend on-wing time using minor workscopes.” He then ends with sound advice, acknowledging that “It’s important to note that the lowest LLP in the stack defines the engine’s remaining service life so our team finds ways to align LLP consumption with performance deterioration for maximum economic efficiency.”

To round things off, Bruce Ansell, Technical Manager Engine Division, APOC Aviation, Lee Carey, CIO, EirTrade Aviation, Andrew Storch, VP Asset Management, Setna iO and Guillermo Soto, Director- Pricing and Evaluation, Enterprise Asset Management Team, StandardAero have additional, more succinct thoughts on the matter. “LLPs have hard limits which determine replacement, while other components have soft limits and are generally replaced on condition, or to match LLP limits. Effective planning is a key factor in optimising shop visit timing and avoiding unnecessary maintenance events, suggests Ansell, while Carey feels that: “LLP limiters are one of the primary reasons for engine removals and engine shop visits. In many instances operators will aim to align LLP replacement with performance restoration.” “Successful engine maintenance planning is optimising for cost minimisation while maximising the performance of the engine, all within the constraints of the LLP life limits. Said differently, the asset owner wants the engine to burn the least amount of fuel for as long as possible, with the upper bound of time on wing represented by the lowest LLP limiter,” Storch adds into the mix, while Soto concludes the responses: “LLP planning is key for operators in two respects: stub life optimisation, that is to say making the most of the LLP life in an engine, to avoid wasted value; and determining the correct mix of new (or part-life) LLPs being incorporated during overhaul, in order to meet the operator’s specific operational needs while minimising MRO spend.”

What are the risks of mixing LLPs with significantly different remaining cycles?

Here we wanted to find out if there is a price to pay for mixing LLPs which had differing life cycles, or if there was a solution that could limit potentially unnecessary shop visits.

Dave Hobbs is quite blunt in his response. “Mixing LLPs with uneven remaining life creates inefficiency across the entire engine. The most immediate risk is premature shop visits. A single low-life LLP can dictate removal timing, even if the rest of the stack still has significant usable life. That leads to more frequent maintenance events and unnecessary cost. There’s also a compounding financial impact. Repeated disassembly, replacement and rebuild activity increases maintenance spend and reduces overall efficiency. From an asset perspective, it weakens market appeal. Engines with non-uniform LLP stacks are less attractive to buyers and lessors. In cases where high-life LLPs sit within an engine nearing the end of its operational life, the cost per cycle rises sharply – high investment, but limited time on wing.” He then sums up the situation very clearly: “Consistency across the LLP stack isn’t just a technical preference, it’s key to maintaining value and controlling cost.” Bruce Ansell is little different to Hobbs in terms of making the pitfalls abundantly clear, warning that: “This runs the risk of throwing money away. LLPs must be replaced upon reaching their life limits; if they are mismatched then the engine will be removed at the lowest limit, leading to decisions about changing those LLPs with remaining life to avoid another costly shop visit in the near future. It is rare for LLPs with sub-5K CR to realise their true value if removed. APOC actively helps customers mitigate these issues trough better lifecycle alignment.”

Being cautious seems to be a recurring theme where responses are concerned. On a slightly different tack, Lee Carey suggests that: “Mixing LLPs with significantly different remaining cycles can be the cause of driving a future shop visit sooner due to a lower LLP limit. Furthermore, this can have a significant impact on the cost of the shop visit, by resulting in the need to replace more LLPs during the next shop visit depending on the engine build standard and hinder the ability to manage the stub life as the engine matures.”

Mixing LLPs with very different remaining cycles creates a structural imbalance in the engine’s lifecycle that almost always shows up later as higher cost, compressed shop visit timing, and reduced flexibility. When one or two LLPs sit far below the rest of the stack, they become the pacing items that dictate when the engine must come off wing, even if every other module still has meaningful life left. For smaller and midsize operators and lessors, this imbalance can force premature removals, disrupt cash flow planning, and undermine the ability to align shop visits with lease return or fleet retirement timelines suggests Virgil D Pizer. He then continues: “When a single LLP is significantly lower than the rest, it becomes the limiting factor that pulls the entire engine into the shop early. This means operators may be replacing or restoring modules that still have substantial life remaining simply because one part has reached its limit. The result is a visit that is technically necessary but economically inefficient. A wide spread between LLP cycles often leads to “stranded life” — remaining cycles on high life LLPs that cannot be fully used before the next removal. That unused life represents sunk cost, especially when LLPs were recently replaced or sourced at a premium. Over time, repeated mismatches compound into higher lifecycle cost. Engines with balanced LLP cycles allow operators to choose between full restorations, partial stack replacements, or green-time strategies. Engines with mismatched cycles lose that flexibility. The lowest cycle LLP dictates the workscope, and operators may be forced into a deeper visit than they would otherwise choose. Especially, lessors rely on predictable LLP cycles to manage mid life transitions and redelivery conditions. A mixed cycle stack complicates valuation, increases the risk of redelivery shortfalls, and can force a lessee into an unplanned visit to meet contractual minimums. For operators, this can mean absorbing a major LLP cost at an inconvenient point in the aircraft’s lifecycle.” He rounds off his comprehensive response by telling us that “Engines with uneven LLP cycles are more vulnerable to unplanned removals becoming economically disruptive. If an unscheduled event occurs close to the expiry of a low cycle LLP, the operator may be forced into a full visit earlier than planned, accelerating spend and reducing the ability to use green-time or teardown-based alternatives.”

“My understanding is that the real risk of installing lower cycle LLPs alongside higher cycle LLPs is that the engine is driven off wing while it is still performing well, i.e., producing low EGT margin but needs removal due to LLP limit. Additionally, an asset owner may inadvertently pay for extra cycles on certain LLPs that will not ultimately be used if the engine is driven off wing earlier than anticipated,” Andrew Storch advises with a cautionary tone. Gullermo Soto would also appear to be of a similar mind to everyone else when he considers the “… biggest risk associated with mixing LLP with dissimilar cycles remaining (CR) is that of hitting a life limit for a single part only, thereby necessitating a premature shop visit (and, potentially, wasted stub life). This risk highlights the need for LLP CRs to match as closely as possible, in order to maximise maintenance efficiencies.”

What are the most common findings during audits related to LLP documentation?

Here we suspected it would be all about traceability and repercussions if paperwork wasn’t complete, but there is clearly more to this question than might be anticipated.

Lee Carey gives as a clear overview of the situation, as he explains: “The minimum technical paperwork requirement from an airworthiness perspective differs greatly to the standard which the market requires from a commercial perspective. In almost all circumstances, EirTrade witnesses that the requirement of the market is far more arduous from a commercial perspective.” He goes further, adding that: “When a used LLP is being sold, buyers expect to receive full commercial traceability for each LLP including the commercial history of the engine(s) in which the LLP has been prior installed. This becomes very burdensome when an LLP has previously operated in another engine to which the owner of the current engine does not have access to the technical records. While this LLP can technically be fitted without the commercial trace of the original engine, most buyers will reject the unit, as they would expect the full traceability of the LLP and any engines in which it was prior installed.” Dag Johnsen is particularly knowledgeable where the CFM56 engine is concerned, telling us that: “In the CFM56 world – where engines often change hands multiple times – data integrity degrades over time. Across audits (regulatory, lessor, or customer), Aero Norway sees the same LLP documentation issues arise frequently. Documentation quality can directly impact whether an LLP is usable – or scrap. These include gaps in back-to-birth traceability; mismatched physical serial numbers and records; cycle accumulation errors (especially after engine/module swaps); missing shop visit release documentation (8130 / EASA Form 1); poor tracking of piece-part exposure during previous repairs.”

Virgil D Pizer provides a very comprehensive response where he identifies the most common ‘repeat offences’ and the cause of the problem. “Audits of LLP records tend to surface the same recurring issues, and almost all of them trace back to gaps in traceability, incomplete historical data, or inconsistencies between what is documented and what the engine has actually experienced. For smaller and midsize operators and lessors, these findings matter because LLP documentation is often the deciding factor in whether an engine can be inducted for a shop visit, accepted at redelivery, or valued accurately during a transaction. The most common finding is a break in the chain of custody for one or more LLPs. Our audits frequently encounter missing birth records, incomplete ownership transfers, or gaps in the documentation that should link each LLP from manufacture to its current installation. Even a small break in this chain can render an LLP unusable or significantly reduce its market value. Audits often reveal discrepancies between operator logs, maintenance tracking systems, and shop visit records. These inconsistencies can stem from manual data entry, legacy system migrations, or changes in utilisation patterns. When cycle counts don’t align across documents, auditors must assume the highest plausible value, which reduces remaining life and can trigger unplanned removals. LLPs that have been swapped, re installed, or transferred between engines require precise documentation of each event. Our audits often uncover missing installation/removal tags, absent shop visit workscopes, or incomplete teardown reports. Without these, the LLP’s remaining life cannot be validated. It is not uncommon to find mismatches between the physical LLP installed, the part number listed in the records, and the configuration required by the latest service bulletins. These errors create uncertainty about airworthiness and can delay shop visits or lease transitions. Even when records exist, they may not meet the formatting, certification, or regulatory requirements expected by operators, lessors, MROs, or authorities. This includes missing authorised signatures, improper document formatting, or lack of required endorsements.” He then concludes: “Auditors sometimes find LLP documentation that does not match the engine’s current module configuration, especially after partial stack replacements or green-time strategies. This misalignment can complicate planning for the next shop visit and reduce confidence in the engine’s lifecycle data.”

Andrew Storch comments on an area of concern not highlighted by others but certainly important, and that relates to a specific scenario where ownership of an aircraft is being transferred. As he points out: “Setna Asset Management has occasionally seen insufficient documentation when assets transfer ownership under distressed financial situations, for example, when an operator goes bankrupt and the assets go into receivership. This tends to be more common with older assets, as the industry has generally improved its recordkeeping practices. In these instances, phase in/phase out documentation may be lost and there may exist gaps in non-incident statement coverage.” Bruce Ansell more succinctly identifies several key areas that clearly are not on-off events, advising that: “Full back-to-birth trace is required, often there are problems with incorrect calculations if the engine has operated at different thrust ratings, or is missing history due to ferry flights, engine swaps, and similar.”

Guillermo Soto brings responses to a close with confirmation of common findings, which he informs us “… tend to be incomplete back-to-birth (BTB) traceability, for example due to missing or incomplete records, and data discrepancies within the documentation. These are often accidental errors relating to incorrect cycles or hours having been recorded, or incorrect engine variant (or thrust rating) information having been recorded.”

How important is the secondary market for LLP sourcing?

With it being next to impossible to schedule all elements of aircraft maintenance around expiry dates or cycles for LLPs, one of the many challenges for MROs is deciding on the optimum time for scheduled maintenance and the replacement of LLPs despite them not having reached the end of their life. We wanted to discover how strong the market is for used serviceable LLPs and what influence that may have on maintenance scheduling decisions.

At AerFin Dave Hobbs provides several reasons why the secondary market has great value in terms of problem solving. “The secondary market plays a critical role in how the industry manages LLPs. It offers a more cost-effective alternative to OEM supply, allowing airlines, lessors and MROs to access material at a significantly lower price point. That has a direct impact on maintenance budgets and overall asset strategy,” he tells us, adding that: “Beyond cost, it also provides flexibility. Operators can extend engine life and respond more dynamically to maintenance requirements without being fully reliant on new production. This becomes even more important during periods of OEM constraint. With ongoing supply chain challenges and long lead times, the secondary market helps keep fleets moving by ensuring material remains available when it’s needed.” Aero Norway’s Dag Johnsen and APOC Aviation’s Bruce Ansell both go one step further, using the term ‘critical’ where the importance of a secondary market for green-time LLPs is concerned. “As Aero Norway specialises in CFM56 engine MRO, the secondary market is absolutely critical. The large global fleet is mature, operators are cost-sensitive and new LLP pricing from the OEM is high relative to engine value. We rely heavily on USM (Used Serviceable Material) and without this market, shop visit costs would increase making many older CFM56 engines uneconomical to maintain,” Johnsen advises, while Ansell also highlights the value of used LLPs for end-of-lease aircraft. “USM is critical for finding LLPs with correct matching life to suit any installed or planned LLP changes; part-life LLPs are also installed to match the expected OH life of the engine. If the engine is leased, there are lease return conditions to be met, these often state how many flight cycles should be remaining on the LLPs. APOC works with several operators who now consider this requirement and plan for replacement well in advance of any shop visit,” he says.

Lee Carey at EirTrade makes a useful reference to LLPs for older engines, noting that: “EirTrade would observe that the secondary LLP market is hugely important as it allows engine owners access to LLPs for shorter build standards, rather than the need to install new LLPs. For more mature engines this can be important when trying to utilise the stub life of an engine whereby a shorter cycle build may be required on one module within the engine to maximise utility from the rest of the engine.” In a similar manner to Carey, Andrew Storch at Setna iO looks at less obvious areas where green-time LLPs have tremendous advantages over brand-new ones, pointing out that: “Secondary market LLP availability facilitates increased asset owner optionality, both financially and technically. Operators and asset owners can save money by not over-building power plants for which there exist plentiful LLPs on the secondary market. This is particularly true for twin-aisle legacy platforms which may only operate a fraction of typical single-aisle utilisation, so asset owners may opt to install lower-cycle LLPs sourced from the secondary market for extra insurance that the engine will perform as planned right up until the cycle limiter.”

At Pem-Air, Virgil D Pizer acknowledges the huge importance of the secondary market for LLPs, but exercises caution owing to supply and demand problems, especially for ageing engines. As he explains, in detail, “The secondary market has become imperative for LLP sourcing because it is the only place where operators can reliably find life-limited parts at prices and cycle ranges that match the realities of aging engines. New OEM LLPs are expensive, often out of proportion to the remaining economic life of the aircraft, and lead times remain long. In today’s environment—defined by tight teardown supply, elevated shop visit demand, and operators holding onto aircraft longer than planned—the secondary market is the practical backbone of LLP strategy. The current market is short on mid-life teardown engines, which limits the availability of LLPs with usable remaining cycles. At the same time, shop visit volumes remain high across several mature platforms, pushing more buyers into the same constrained USM pool. This imbalance drives volatility in pricing and makes it harder to source LLPs with the right remaining life. For many operators, the secondary market is no longer just a cost-saving option—it is the only viable path to keeping engines serviceable without committing to uneconomic full stack replacements. Aging engines rarely justify installing brand new LLPs with full a lifespan. What operators need are LLPs with remaining cycles that match the aircraft’s planned horizon, whether that’s a short bridge to retirement or a few more years of service. Only the secondary market provides this range of life options. Without it, operators would face stranded life, premature removals, or shop visits that no longer make financial sense.” He then concludes: “PMA has already replaced many LLPs on certain platforms, and where approved, it can be a powerful stabiliser in a tight market. PMA LLPs offer more predictable pricing, shorter lead times, and independence from OEM supply constraints. In environments where teardown flow is thin and USM pricing is inflated, PMA can restore economic balance by providing new life LLPs at materially lower cost. For operators managing mature fleets, PMA can be the difference between extending an engine’s life economically and retiring it early.” Meanwhile, at StandardAero, Guillermo Soto is succinct in his assessment of the situation: “The secondary market is extremely important for LLP sourcing, especially for those operators looking to short-build an engine for a specific number of cycles or hours. Access to used serviceable material (USM) enables operators to avoid potentially wasted investment in zero-time material when it’s not required,” he concludes.

What pricing dynamics influence LLP trading?

As with so many aspects of parts’ management, there are several differing factors which can affect the value and pricing dynamics of LLPs, and we wanted to learn a little more about what has the greatest influence.

Here Virgil D Pizer and Dag Johnsen both identify the same three clear factors. “We at Pem-Air see that pricing in the LLP market is shaped by a few predictable forces that interact with each other: supply scarcity, platform maturity, and the remaining cycles on the part itself. The tight teardown pipeline keeps mid life LLPs in short supply, which pushes prices up—especially for high demand disks and hubs on platforms with heavy shop visit activity. At the same time, OEM list prices continue to rise, creating a wide gap between new and secondary market material and anchoring USM pricing at elevated levels. Cycle life is the final driver: LLPs with “right sized” remaining life command a premium because they allow operators to match spend to their remaining service horizon, while full-life or very-low-life parts trade at discounts due to limited applicability. These dynamics make LLP pricing highly sensitive to timing, platform-specific demand, and the availability of teardown engines,” says Pizer. In turn, Johnsen backs this up, saying: “LLP value is directly proportional to remaining cycles but heavily adjusted for market demand and documentation quality. Full LLP sets can command a premium, whereas ‘odd-life’ parts are harder to place and discounted. Aero Norway sees that LLP pricing is very dynamic and focused on remaining cycles, engine variant demand, teardown supply, traceability quality.” Dave Hobbs agrees with both Pizer and Johnsen in identifying the three key factors affecting price, but adds to that when he tells us that: “Remaining cycles is the most influential. The more life left in a part, the higher its value. Engine type also plays a key role. LLPs from active, in-demand platforms typically command stronger pricing due to consistent utilisation and demand. Availability is another factor. Scarcer material will naturally achieve a premium, particularly where sourcing options are limited.” He then adds that “Interchangeability can work the other way. Where LLPs are widely interchangeable and readily available across platforms, increased supply can soften pricing, while concluding: “Finally, documentation matters. Strong back-to-birth traceability, particularly for first-run or single-operator parts, supports faster transactions and often commands a premium.”

While there may be a number of factors affecting the value of LLPs, Andrew Storch feels that pricing is relatively predictable, pointing out that “LLPs are arguably some of the most predictable parts in terms of pricing and availability, since their value always behaves as a function of variables such as scrap rates, published list price, and life-limits. Further, LLPs are very rarely found to be “beyond economical repair,” or BER, since the repair costs are usually a fraction of the list price. Generally, the highest-demand LLPs are the ones that support the largest fleets and have the highest scrap rates. LLPs with the lowest yields are usually found in the hottest sections of the engines, namely the high-pressure turbines, followed by the high-pressure compressors, followed by the front stages of the low-pressure turbines.” Guillermo Soto also has some interesting points to make in terms of engine types and aircraft models, telling us that “The current level of demand for a specific engine type will obviously influence LLP pricing (and demand), as will the availability – or lack thereof – or new parts. These dynamics have been particularly noticeable in the market for CFM56 and V2500 LLPs in recent years, reflecting the strong demand for Airbus A320ceo and Boeing 737 NG aircraft, and the low level of retirements.” To conclude, Lee Carey has some key observations to report. “LLP pricing in the context of used LLPs is a function of supply, demand, and the list price of a new unit. LLPs typically increase at a rate of 6% however, in recent years, EirTrade has noted that the annual Catalogue List Price increase has far exceeded this,” he notes.

What advice would you give to technical directors managing aging fleets?

Delays in aircraft deliveries are not only frustrating for carriers, but they have exacerbated an already existing shortfall in available USM, including LLPs, especially for certain engine types. With more and more aircraft remaining operational beyond their anticipated retirement age, we wanted to know how technical directors were handling the situation.

Bruce Ansell has sage words, advising: “Firstly, assess how long you need the engine to remain flying, then identify what parts and maintenance are likely to be required to reach this target, and finally, investigate what parts are available in the market and at what price. If your plan is fixed, it is always worth reserving or buying the right components when they are available, otherwise you run the risk of low availability and higher prices when the parts are needed. Suppliers like APOC support operators throughout this process, helping secure the right components at the right time.” Dave Hobbs is equally enlightening as he suggests: “Start with a clear view of the engine’s remaining operational life. That defines the build goal and shapes every decision that follows. From there, planning becomes critical. Align the work scope with that end goal, select the right MRO partner early, and secure material in advance.

Pre-purchasing LLPs and other components gives you greater control – over availability, pricing, and the time needed to properly review documentation. In aging fleets, reactive decisions are costly. A forward-looking approach allows you to manage risk, control spend and get the most out of the asset.”

Andrew Storch is very committed and has gone ‘all in’ on one specific aspect of parts’ inventory, as he comments: “Throughout my career, adoption of used serviceable material (USM), including LLPs, has seemed to monotonically increase year over year. This is due to the impressive reliability of component MROs’ products, and the substantial cost savings of USM compared to factory new list pricing. I cannot recall a technical director that was not happy with his or her decision to onboard more USM, and I would advise ageing fleet managers to increase their adoption of USM to improve the financial performance of their fleets.” Further sound advice comes from Virgil D Pizer, especially in terms of being proactive, as he explains: “Technical directors managing aging fleets benefit most from treating LLP exposure as a forward-looking economic signal rather than a reactive maintenance item. The engines that stay reliable and affordable late in life are the ones whose LLP cycles, documentation, and sourcing strategy are planned well ahead of the next shop visit. That planning starts with mapping remaining LLP life against the aircraft’s intended service horizon so the workscope matches the value of the asset—full restorations when the aircraft has years ahead, targeted module work or partial stacks when it doesn’t, and green time or teardown-based solutions when LLP investment no longer makes sense. Aging fleets also depend on clean, defensible documentation. LLP traceability gaps remain one of the most common and costly audit findings, and even small breaks in back-to-birth records can delay shop visits or reduce asset value. Directors who maintain disciplined cycle tracking and complete installation/removal histories avoid those surprises and keep their engines eligible for induction, transition, or sale. Market conditions make sourcing strategy just as important. Tight teardown supply and elevated shop visit demand have pushed mid-life LLPs into short availability, so securing the right parts early—well before a visit is due—helps avoid last minute procurement at inflated prices. PMA LLPs, where approved, now play a meaningful role in stabilising cost and availability, offering new life parts without OEM premiums and helping operators extend service life economically when USM is scarce.” He rounds things off by suggesting that: “The most effective directors align workscope depth with economic reality, using flexible, lifecycle-appropriate maintenance rather than defaulting to full restorations. That balance—technical condition, remaining cycles, and financial horizon—is what keeps ageing fleets viable.”

Guillermo Soto has two recommendations, and that is: “to plan ahead, especially for those engines in high demand where LLPs may have a long lead-time, and work closely with your MRO provider, since they will have experience in matching operator requirements to shop visit schedules, along with an extensive network of LLP suppliers.” To then conclude this article on engine LLP management, Dag Johnsen is quite clear. “From Aero Norway’s hands-on MRO experience, these are our words of advice: collaborate early with your MRO. The best outcomes happen when LLP planning is done before induction, not decided mid-shop visit, when costs can escalate. We advise operators to plan engines as complete life packages and align LLP life with performance life. Do not install very low-life LLPs just to defer costs, make sure you target a balanced exit condition after a shop visit. Try to use the secondary market strategically and buy LLPs when market is soft – this avoids panic buys during an AOG or capacity shortages. Importantly, protect your records like assets. Good LLP paperwork has real monetary value, but poor records can destroy resale or lease return value. Segment your fleet, some engines should be run to part-out, others require investment in LLPs to extend life.”